A Detailed Guide by Paisa Sarthi

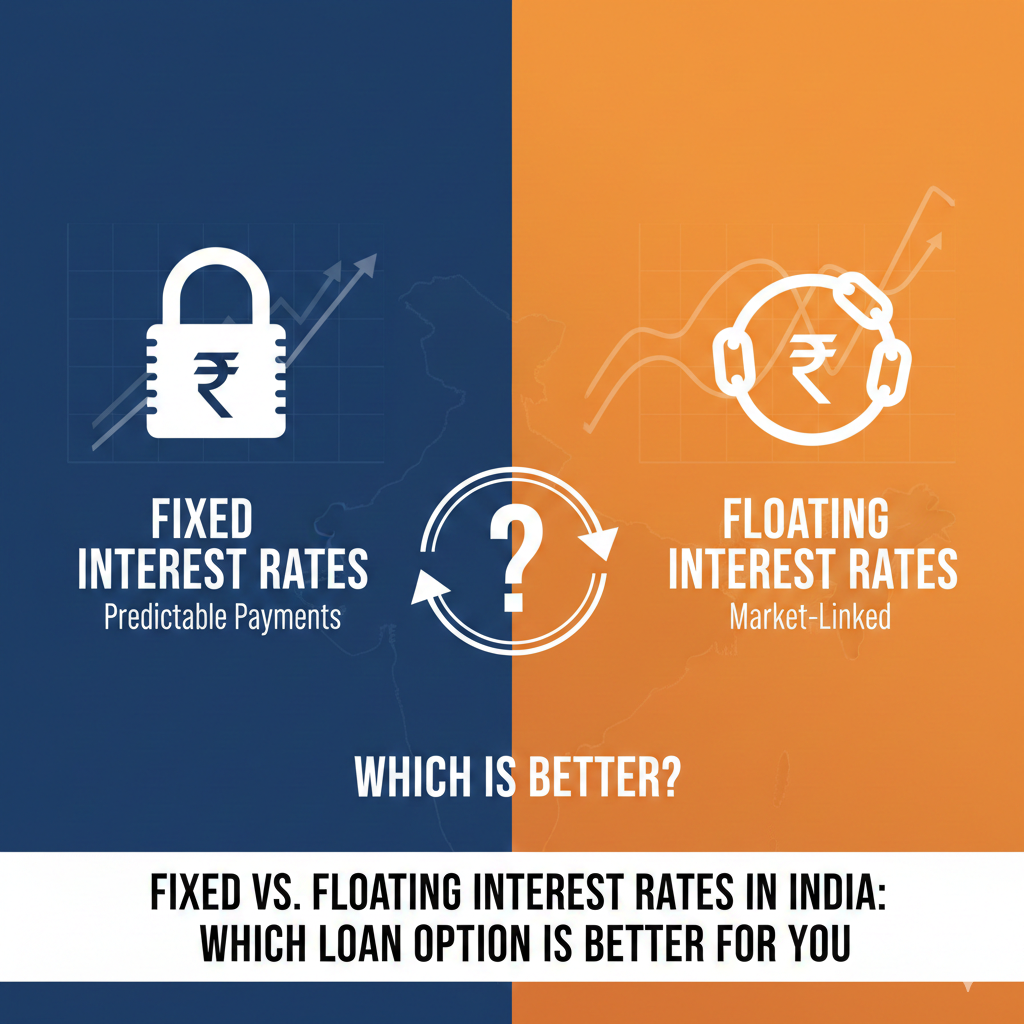

When applying for a home loan, business loan, or even a large personal loan, one of the biggest decisions you’ll face is choosing between a fixed interest rate and a floating interest rate.

This choice directly affects:

- Your monthly EMI

- Total interest paid

- Financial stability

- Long-term savings

In this detailed guide, Paisa Sarthi explains everything you need to know about fixed vs floating interest rates in India — so you can make a smart, informed decision.

What Is a Fixed Interest Rate?

A fixed interest rate remains constant throughout the loan tenure (or for a fixed initial period).

This means:

- Your EMI remains unchanged

- Interest rate does not fluctuate with market conditions

- You get predictable repayment planning

Many borrowers prefer fixed rates for stability, especially during uncertain economic conditions.

Major lenders like HDFC Bank and ICICI Bank offer fixed-rate loan options with specific terms and reset clauses.

Advantages of Fixed Interest Rates

✅ Stable EMIs

✅ Better financial planning

✅ Protection from rising interest rates

✅ Peace of mind during inflation cycles

Disadvantages of Fixed Interest Rates

❌ Higher initial interest rate

❌ Limited benefit if market rates fall

❌ Prepayment charges may apply

Fixed rates are usually 0.5%–1.5% higher than floating rates at the time of sanction.

What Is a Floating Interest Rate?

A floating interest rate changes based on market conditions and benchmark rates.

In India, most floating loans are linked to the RBI’s repo rate.

The benchmark is set by Reserve Bank of India.

When the RBI increases repo rates:

→ Your loan interest rate may increase

→ EMI may increase or tenure may extend

When the RBI reduces repo rates:

→ Your interest rate may reduce

→ You save on total interest

Banks like State Bank of India link many home loans directly to repo rate benchmarks.

Advantages of Floating Interest Rates

✅ Lower initial interest rate

✅ Benefit when interest rates fall

✅ Usually no prepayment penalty

✅ Better for long-term loans

Disadvantages of Floating Interest Rates

❌ EMI uncertainty

❌ Budget planning becomes difficult

❌ Risk of higher payments during rate hikes

Fixed vs Floating: Key Comparison

| Factor | Fixed Rate | Floating Rate |

|---|---|---|

| EMI Stability | Stable | Variable |

| Initial Interest | Higher | Lower |

| Risk | Low | Moderate |

| Benefit During Rate Cut | No | Yes |

| Best For | Short-term certainty | Long-term savings |

Which Option Is Better for You?

There is no universal answer. It depends on:

1️⃣ Loan Tenure

- Short tenure (3–5 years): Fixed may be safer

- Long tenure (15–30 years): Floating often more beneficial

Most home loans in India run 20+ years, making floating rates popular.

2️⃣ Interest Rate Cycle

If interest rates are already high and expected to fall:

→ Floating rate is usually better

If rates are low and expected to rise:

→ Fixed rate may protect you

Understanding economic trends matters.

3️⃣ Your Risk Appetite

If you prefer:

- Stability

- Predictability

- Fixed budgeting

Choose fixed.

If you are comfortable with:

- Market fluctuations

- Some EMI variation

- Long-term savings strategy

Choose floating.

What Most Indian Borrowers Choose

In India, nearly 70–80% of home loan borrowers prefer floating rates because:

- Lower starting interest

- No foreclosure charges

- Long tenure advantage

However, each case is different.

Hybrid Loan Option (Best of Both Worlds)

Some banks offer hybrid loans:

- Fixed for first 2–5 years

- Floating thereafter

This helps you:

- Stay protected initially

- Benefit from long-term market drops

Always check reset clauses carefully.

Important Questions to Ask Before Choosing

Before finalizing your loan, ask:

- Is the fixed rate truly fixed or reset after 3–5 years?

- What benchmark is the floating rate linked to?

- Are there foreclosure charges?

- How often does the rate reset?

- Will EMI increase or tenure increase during rate hikes?

These details matter more than just the headline interest rate.

Real-Life Example

Suppose you take a ₹50 lakh home loan for 20 years.

Fixed Rate: 9%

Floating Rate: 8.5%

Difference: 0.5%

Over 20 years, even a 0.5% difference can result in savings of several lakhs — depending on rate movements.

Small percentage changes make a big financial impact over long tenure.

Paisa Sarthi’s Expert Recommendation

At Paisa Sarthi, we analyze:

- Your income stability

- Loan tenure

- Market trends

- Risk comfort level

- Repayment capacity

Then we recommend the best structure for you.

Choosing between fixed and floating is not just about today’s rate — it’s about long-term financial strategy.

Final Thoughts

Both fixed and floating interest rates have advantages.

The best choice depends on:

- Economic outlook

- Loan tenure

- Financial discipline

- Personal comfort with risk

Before signing any loan agreement, understand every clause carefully.

Smart borrowers compare.

Smarter borrowers seek guidance.

If you’re planning a home loan or business loan, Paisa Sarthi can help you select the right structure and lender — ensuring you save money and reduce financial stress.